Sorry everyone for the tardy delivery of the blog. But I have some bad (good?) news for you.

As many of you know, I have been wrestling with this for a while, but I have decided, after much contemplation and consultation with loved ones and colleagues to call an end to the blog after this week. After all, I am running out of things to talk about, what with the ills of the energy sector being solved by our Liberal Party of Canada overlords and the wise men of OPEC (+). I mean, think about it, why read this nonsense when there are people oh so much smarter than me around to tell you what to believe about the sector. Never mind that the sector is about to come to a crashing halt once the Federal government passes all its energy industry destroying bills. And that there are elections coming up in the province of Alberta, Canada and of course the total gong show that will be Trump 2.0 in 2020.

Even with all of that, I just can’t do it anymore. The inspiration is gone. So I want to thank everyone for tolerating my ranting and slagging and all that I have done over the last four years. I feel in some ways that my job is done.

I was going to send this on Friday but my wife convinced me to take the weekend to think about it and send the blog today. And the decision stands. This is the last blog.

At any rate, one last hurrah for old times’ sake, right? How about it? Who’s with me?

And as luck would have it, it’s the end of Q1 so it’s report card time for the fearless forecast.

So, it’s been an interesting first quarter hasn’t it? I mean aside from the obvious stuff with Trump and Trudean and SNC Lavalin and election calls and Kamikaze candidates and leadership ballot stuffing. It’s been eventful enough to fill, I don’t know, three months’ worth of blogs.

And now that the Mueller Report is in various stages of being released and/or leaked, we no longer have as much fun of a Trump Watch… or do we? Trudeau is on the run and Conservatives everywhere in Canada still have only a very slim chance of forming a government.

It’s all very weird, but as we all know, I forecasted all of this in my year-end Fearless Forecast, even the swirling madness that is the price of oil… Didn’t I?

Well let’s find out.

Broad Themes

The forecast for this year started with civil unrest, particularly in the Middle East, which, now that I think about it a bit was a giant cop out. After all, what could be easier than predicting unrest in Iran, Iraq, Israel, Palestine, Yemen and other places, especially with US sanctions biting in Iran, Syria doing that Syria thing, ISIS being defeated, Turkey and Russian meddling. The usual. So a bit of a cop out of a forecast even though it is pretty much spot on every year. In fact it is the easiest forecast one can make in geopolitics.

And of course it does playout as it is supposed to month after month, year after year. And, not to be outdone this year we have the Indian subcontinent getting active with Pakistan and India deciding to trade a few upper cuts over the Kashmir.

While the conflict in India flared out fairly quickly, the fun in the Middle East is percolating and promising to entertain for the balance of the year.

The other theme I discussed was the unfolding global economic slowdown and the rising recession risk in North America and Europe as well as a trade and debt induced economic shock in China. Recent indicators in North America are mixed but policy makers are rightly freaked out about inverted yield curves in both Canada and the US. Industrial production and trade numbers indicate some underlying weakness and are trending downward, but have not yet breached soft landing territory. However, the combination of massive corporate and government debt and persistent deficits, unnecessary and unproductive trade wars and the flashing red warning signals the stock market is giving should give everyone pause. And as bad as the numbers may look out of the US, the European and Chinese indicators are all much, much worse. Current recession risk in the United States is rising and in Canada some economists suggest we are already in one. China has just reduced its economic growth forecast to less than 6%. Things are not very stellar out there.

The other prediction I made was that the Donald Trump trade war would come to an end so that the world can recover some semblance of an even keel. Is it happening? Not as fast as it should but at least China and the United States are in negotiations although, true to Trumpform, there are a lot of announcements and very little in the way of progress. As I said in my forecast, I have zero confidence in the ability of anyone involved to extricate us from this madness so, as I said, buckle up.

The next part of the qualitative forecast is harder to assess. I suggested that 2019 was going to be hard for the Donald and I still believe this to be true. He has lost the House and can no longer govern via executive order with impunity. Nancy Pelosi is a more than capable check on the Trump and the Democrats have the GOP on the run in many areas. With the economy slowing, no one believing in the border wall emergency and the White House suddenly refocused on bankrupting middle class Americans via health care, it would seem the deck is stacked. But then the Mueller report gets released, a suspect summary is released and it seems like the Donald is, for now at least, off the hook on Colluuuuuuusion. For now. Part of the way in to the year, the White House is in flux and it’s hard to say who has the upper hand.

On the energy front, my predictions really centered around the lack of exploration being initiated outside of the Permian and the day of reckoning that is coming. With OPEC+ finally taking the supply side seriously and Saudi Arabia determined to jack up the price of oil, that lack of investment should come to everyone’s attention with increasing force as the year progresses. Except in Canada. We are a basket case. Let’s all hope OPEC has some spare capacity when it is called on in Q4.

Thematic Grade? B. Directionally OK, but still a work in progress.

Production

Our prediction on production is of course area dependent but as always starts with the madness that is the Permian, West Texas and the rest of shale-mania. Our forecast was increased production in the United States of up to 800,000 bpd, closing the year at 12.5 mm bpd.

I think we can still get there, but the first quarter was, for want of a better term, a dud. Drilling rigs were off in the United States in Q1 by the most in several years as operators paid lip service to capital discipline and instead focused on reducing the number of DUCs. And a funny thing happened on the way to the oilfield – initial production rates are taking it on the chin, child wells are a growing problem and well spacing is being expanded on the fly. Activity continues to expand in the Gulf though, as predicted, potentially offsetting any speedbumps in the Permian.

US production closed the quarter at 12 million bpd, realizing more than 25% of the year’s predicted growth but expect that number to stagnate for a while.

US Production Grade – B. A decent start, but with elevated prices, the forecast may fall short.

In Canada, notwithstanding current curtailment policy, we predicted modest growth in production – on par with last year, probably in the order of 250,000 to 300,000 bpd of oil. This will come from both oilsands, the conventional world and condensate. And it’s going to come in the second half of the year. Not while production is curtailed.

Canada Production Grade – Incomplete.

An aside about curtailment. Our prediction was that the curtailment job is done, time to get out of the way and let the market finish the job. Only time and the election in Alberta will answer this forecast.

Curtailment Grade – Incomplete

OPEC production levels were predicted to be flat year over year depending on what happens with the new OPEC/NOPEC agreement at the various jump-off points through the year. The key to the agreement is the Saudi/Russia collaboration continuing at least until June. We now know that the April review meeting has been scrapped and the Saudis are producing well below their quota in a bid to rapidly restore balance.

Grade – A

The rest of the world was supposed to see limited growth this coming year. A lot of projects making noise (Brazil, Mexico) but they are years out from making a dent. Interesting to hear China announce some new investment in their tired oilfields, but they likely see the writing on the wall.

Price of oil

As always the glory call. And this year I went bullish is as bullish can be because i think the bullish case wins the year. Plus it’s fun to be bold, even if you miss.

I truly think the bullish case for prices wins, but I predicted oil prices to be pretty volatile during the year. My year end price is $80.03 but my average price for the year is going to be $61.47. At the end of Q1, the price of oil was $60.18 and the average was $54.90. It’s going to be a long year.

Grade C – directionally right but too soon to tell.

Price of Natural Gas

Ah natural gas, I can’t quit you! Super cold winter, massive consumption, LNG and we still can barely catch half a break on pricing. Notwithstanding another massively bullish call, it’s going to be a long year.

My year end price for natural gas is going to be $3.90 and the average price will be $3.26, up marginally from last year. Fingers crossed. At the end of Q1, the price was $2.66 and the average was $2.87.

Ugh. I. Give. Up.

Grade C-.

Activity Levels

On the Canadian side, this year was posited as a hard one to predict given the curtailment policy of the Alberta government, egress issues and all that.

The basic prediction was an unmitigated disaster for Q1, self-correcting through the first half with a rally of sorts in the second hald of the year.

So far so good! Or bad.

The rig count was consistently 30% below last year’s levels through Q1 and an early breakup has flat-lined activity. That said, there are promising signs for H2.

Our forecast was flat with last year and of course we must stick with it. But it’s really too early to tell and if we get one more pipeline disappointment, we may all just move.

Grade D – Not looking good so far

Unlike Canada, the US had significant growth last year in both rig count and production. That said, the rig count has been relatively flat for a number of months. While the Permian land rush continues, we predicted the large inventory of DUCs will hold back the rig count and drilling activity somewhat in the first half. Keep in mind that the Permian has similar offtake issues as Canada, although with a higher will to solve them.

That said, there is still cash coming in and the incentive to drill will always be there, regardless of price or profit since as was widely reported after the Schlumberger year end call – soon 75% of all US drilling will be just to maintain production levels. Ouch.

Grade – C – Incomplete.

M&A Activity

We predicted that M&A activity in Canada would pick up as the curtailment issues settled out and infrastructure got more certainty. And we are sticking to that. For Q2/3 and 4. A number of high quality Canadian assets are in the market and should transact in the next quarter or so. It is impossible to think they won’t with the massive discounts available

Similarly, the services sector should see activity pick up in the second half of the year, certainly on the private side.

LNG construction is under way and it is hard to ignore as an opportunity. Money will follow.

Just not yet.

That said, Canada is a currency advantaged, rational valuation and stable market for consolidators tired of the madness in Texas. BUY, BUY, BUY.

Grade D – Incomplete

Canadian Dollar

The Canadian dollar should see some relative stability this year with the commodity price, but a slumping economy is going to counterbalance that. We are currently at $0.75 and I predicted $0.78. We need an actually growing energy sector to get there, so the fingers are crossed.

Grade B

Infrastructure

I know on the surface things look bleak, but it may surprise people outside of the energy sector that we are on the cusp of an infrastructure supercycle in Canada and I still believe that. This should continue well into the 2020s. Out on a limb and don’t fit me for a straight jacket, but I fully expected to see the following in 2019:

- Line 3 complete and operational by year end (oops)

- TransMountain Expansion underway in the summer (likely)

- Keystone XL back in play later this year (promising)

- Coastal Gas Link fully underway this summer (yup)

And we may get one more LNG FID this year. So there.

Grade C

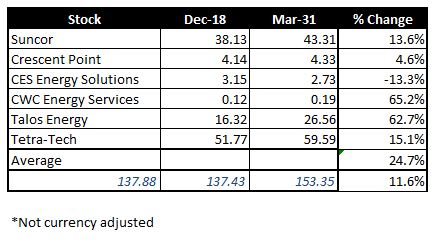

Stock Picks

Since last year was such a disaster, I decided to pick some names I was more familiar with and also a few… outliers. Still not sure of the wisdom of this, but it was worth a shot.

True to my rules, this year I pick two Canadian E&P’s as well as two service companies and, finally, one American producer and one American service company. As a reminder, the companies were as follows:

- Suncor. A core holding if you want to play Canada.

- Crescent Point. The down-trodden once golden child trying to reinvent itself.

- CES Energy Solutions. CES provides chemical solutions and services through the lifecycle of the oilfield ranging from upstream through piplines and downstream.

- CWC Energy Services. Small cap service and I know the CEO and he’s a pretty smart guy.

- Talos Energy. A pure-play Gulf of Mexico producer with current production of 55,000 boe.

- Tetra-Tech. Consulting and engineering in the areas of water, environment and infrastructure.

Here goes nothing…

Wow – not bad. I’m just going to leave it at that.

Oh, and I’ll see you next week with my Alberta election prediction.

April Fool’s suckers – you can’t get rid of me that easily.