Good day everyone, I hope you are all safe and sound and self-isolating to the best of your abilities, I understand it isn’t easy for everyone, jobs are different, some people are on the front lines and others don’t have the luxury of being a home office, cloud based desk jockey like me.

These are truly bizarre and uncertain times and as such, everything appears to be in flux, including where to take this blog on a week to week basis. Last week was about our response to COVID-19 and what we are doing to maintain our business and support clients and stakeholders as we navigate uncharted waters and mixed metaphors.

This week of course could just as easily been more of the same, playing on the theme of what we can do for clients and strategies and ideas and all that stuff, but as I was informed by a couple of people, readers don’t come here for “that”, they come here for contrarian commentary, the occasional sarcastic rant and, to be fair, occasionally a lighthearted distraction.

So that’s where we are going to go. To the best of my abilities, the regularly scheduled programming of Crude Observations is going to continue along the lines of what you are used to.

Accordingly, we will use ad hoc mid-week programming to draw attention more to pragmatic business solutions that our clients and other might consider to assist them in ensuring business continuity as the weeks (and months) ahead unfold.

Interestingly next week is my Q1 report card on my Fearless Forecast which we all know is going to a flaming disaster – I may actually reserve the right to declare Force Majeure and start again from scratch. But then again, part of me thinks it will be way more fun to review and mock how off I was on a quarter by quarter basis and see if, as the year unfolds, the numbers and politics start to converge at some point, or is the reset post coronavirus going to be that much more systemic.

Speaking of resets, US tight oil is where I wanted to dive this week, if it’s alright with all of you.

I have a sneaky feeling, a voice in the back of my head really, that is saying that these thorns in the side of OPEC and Russia, may not be the centre of attention they are used to being for much longer, or if they are, it won’t be for the same reasons.

As everyone in the energy industry knows, Saudi Arabia launched its price war in early March, opportunistically jumping on the Coronavirus induced demand-side meltdown to bring in their own supply side double-whammy, effectively blowing up the OPEC+ arrangement and putting a shiv into the rib cage of the world’s high cost producers, most specifically, Canadian heavy and US light tight oil.

Let’s leave Canada to the side here.

While it has been postulated that this is nothing new and the shale industry has survived this type of crisis before (late 2014 through 2016), the reality is that the market is so much different now.

For much of the past seven years, high cost light tight oil has fed the growth in energy demand around the world, whether displacing OPEC oil coming into the United States or through exports after the United States lifted the export ban in 2015.

But now, with demand expected to plummet over the next quarter by anywhere between 5 and 10 million boepd, all that oil has nowhere to go except into storage or stay in the ground. Some oil prices are already negative at the well-head. Western Canadian Select is trading at the same price per barrel as a pint of socially distanced IPA. Prices for LTO are way down as well.

In addition, as has been well documented, the capital markets have been closed to shale operators for the better part of a year, forcing “capital discipline” and “investing only cash flow”, which was a good thing for an over-leveraged sector in a slow but steady price environment. In fact, as documented here, capex in the United States was expected to be cut by 10%-15% in 2020, well before anyone had even heard of coronavirus. Part of the reason for this is the so-called Debt Wall that shale producers have coming, which refers to the debt maturing over the next 2 or 3 years from the last round of downturn-averting recapitalizations.

So what the producers have been doing is dialling back the growth curve and producing the snot out of existing wells to capture every last dollar.

It was potentially survivable when coronavirus was affecting just Asian demand and it looked like China was getting a handle on things. It was a game of survivor when coronavirus started to spread around the world. With Saudi price war, it’s existential. While many producers say that on a very narrowly defined “operating costs” basis they can make money at these price levels, the reality is that the entire sector is pretty much underwater. In this price environment, the debt wall is insurmountable, production at all costs makes no economic sense and, to many analysts, there is a sense that the party may finally be over.

What do they base this on, aside from the looming debt crisis?

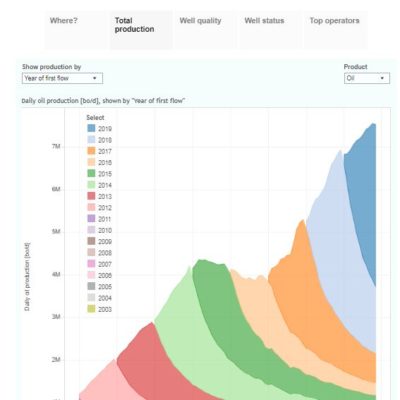

First off, as I pointed out a while back, of the 7.5 mm barrels of LTO per day produced by the US, a full 3.8 mm are from wells drilled and completed in 2019. And these wells have a first-year decline anywhere from 40% to 65%. On top of this, wells with an older vintage are still declining, albeit at a slower rate (generally less and less per year) – let’s call it 25% on average. So, if all drilling stopped tomorrow, a year from now we would have 1.9 mm barrels less of 2019 vintage production (avg 50% x 3.8) and 925k less of pre-2019 production (25% x 3.7). Note that this doesn’t even consider the other 5 mm some odd of conventional and off-shore production the United States has, which has it’s own decline rate.

So that’s a “worst case” of 2.825 mm boepd of production decline out of the United States. How likely is that?

It’s hard to put a precise pin in it, but all signs say we are on the way. Post Saudi price war, US capex budgets have been cut by on average 70%, from budgets that were, as discussed, already 10-15% lower.

It’s not pretty. To put it mildly.

Expectations are that US production is likely to fall by between 2 and 2.5 million boepd this year and further still into 2021.

But what about a bailout? What if prices rally at some point in late 2020, can’t the shale drillers just light the fuse again and get going?

Sure. And they will likely try. But even if the damage is limited to just 2 mm boepd for 2020, to make that up will require the industry to replicate the growth of 2017-18 when money was falling off trees and industry spent a mind-boggling $90 billion.

While investors may take some risk coming out of the trough driven by a motivation to rebuild, pride and a desire to secure energy independence, the consensus (among a group of analysts) is that all the efficiencies have been wrung out of this resource – peak efficiency and peak production. Not to mention that even with zero cost debt, with the wall of maturities coming there is likely to be very little capital available. I have read where some 50% of tight oil companies may go bankrupt.

Does anyone realistically believe that $90 billion will be available to US LTO when Saudi Arabia just needs to issue a press release they can’t possibly back up to sewer the market yet again?

Given all this, it is hard not to believe that US tight oil has likely peaked.

So with the proverbial stroke of a pen on March 7, 2020, Saudi Arabia effectively truncated the tight oil market and restored its supremacy.

Arguably, Saudi Arabia and Russia can now come back to the table and work to stabilize oil prices “out of concern” for the demand issues caused by coronavirus. Because let’s face it, the last thing these two actually want is low prices, they just want market share. Ironically, that is exactly what is happening, led by Russia.

Mission Accomplished, Putin rides bare-chested and bareback to the rescue on his fine Arabian steed.

Sorry for the visual, but there it is.

So What About Canada?

Funny you should ask. Canada is of course swept up in the price war as well and with our discounted crude we are at a distinct disadvantage to others, given our isolation, distance from markets and super expensive to extract crude. It is going to be an extremely rough ride for Canada and I will write about this in subsequent blogs, but for now, I would posit that what is maybe our biggest weakness is also our biggest strength.

Why do I say that? First off, our 4.4 mm boepd energy sector is dominated by long lived, low decline assets whose production is dominated by a relatively small number of players. Plus, we already have curtailment legislation in place to manage production (a luxury that doesn’t exist in the US).

This means that we have multiple levers to help the industry. We can curtail production to reduce differentials and we can provide financial support to producers at the same time and truth be told, it is unlikely that Saudi Arabia or Russia will really care given the costs associated with increasing Canadian oil production, especially oilsands. Their target is and always has been shale, especially after the export ban was lifted in 2015 and shale started to go to China.

In the meantime we can continue to inch along with building out our egress infrastructure – in particular the Line 3 Replacement and the TransMountain Expansion. Perhaps eventually the Keystone XL. This will allow us to continue exporting into the largest and most secure market in the world as well as dip our toe into international exports.

Finally, oil demand will recover once the coronavirus pandemic recedes as 2020 progresses, except this time it will be in an environment of declining LTO production and newly supply managed OPEC+. Under this scenario, some analysts predict that by mid to late 2021, it is likely that we could see an oil supply surplus quickly shift to a fairly sizeable deficit, which, all things being equal, should be of benefit to Canada and a couple of shiny new pipelines.

Hey, it’s a scenario right? Out of the dark we seek light? Silver lining? Just saying.

So if I’m a federal government, about to blow up the national purse to rescue the economy and wondering where the funds are going to come from to ever pay this back, I am looking to double down on the energy sector with financial aid and, as I said in a presentation earlier this week, if ever there was a time to make sure energy infrastructure gets built, it’s now.

Look, it isn’t going to be an easy ride. It’s gonna take nerves of steel and a lot of luck. I will write about that in future blogs. But it is possible to envision positive outcomes. So let’s stay focused.

OK, so Office Cat Week 2, right?

What is your routine? I am afraid I am falling into some weird habits pretty quickly. First off, I don’t get up at the crack of dawn. I haven’t set my alarm since Thursday March 12th.

I get up, I wander downstairs and make a coffee and some breakfast. On occasion there is small human with me – I am told this is one of my kids (just kidding!).

Then I check emails for a bit, catch up on relevant news and get ready for the day. On occasion I have an update call with a client and, depending on whether it’s a video conference or not, I decide how presentable I need to be.

Having been through the work from home deal in a previous life, I’m past the “suit in the home office” phase, but I suppose if someone wanted me to be in a suit, I could.

Office Cat now has a tie and usually joins me around 9:30 to sleep in the sunspot I’ve prepared or surf Twitter over my shoulder. Interestingly enough, we have two cats, but only one is called Office Cat. The other I will call “Client Cat”. She will visit on occasion but never the two at once.

Aside from this, it’s a pretty lonely existence. Like everyone, I am getting used to the video tools and learning how to distance work. For the most part the family has figured out the “dance” but for sure I need to get better at doing my part around the house, which, truth be told, should go without saying. Thankfully the learning curve is short and, given how efficient you can actually be working from home (short commute, few distractions, flexible hours), this is something that can be easily stepped up.

As it currently stands, I work pretty steady in the morning, take lunch, do a bit more after lunch and usually mail it in by late afternoon unless I have a call. So really not much different than a typical work day.

I am sure as the weeks stretch on, there will be ups and downs and many learnings, but humans are ever-adaptable creatures. We will get used to this, likely just in time to head back to the office. Just like the kids will get used to online learning even though they deeply miss their friends.

I personally shudder to think how inefficient a transition back to an office environment will be!

I miss the physical interaction but accept that this is really not much of a sacrifice for the greater, communal good.

I have yet to participate in a video happy hour, but if anyone is up for it, I say bring it on!

I hope all of you and your families are doing well.

Fearless Forecast Q1 report card next week. Oh boy!

Stay safe. Wash hands. Be kind.

Prices as at March 27, 2020

- Oil prices

- Oil storage was up

- Production was down marginally

- Natural Gas

- Storage below last week, but historically very high; consumption down; production flat; exports flat.

- WTI Crude: $21.80 ($23.23)

- Western Canada Select: $5.55 ($9.23)

- AECO Spot: $1.808 ($1.79)

- NYMEX Gas: $1.615 ($1.581)

- US/Canadian Dollar: $0.7130 ($0.6936)

Highlights

- As at March 20, 2020, US crude oil supplies were at 455.4 million barrels, an increase of 1.6 million barrels from the previous week and a increase of 13.1 million barrels from last year.

- The number of days oil supply in storage is 28.9 which is 1.3 above last year at this time.

- Production was down marginally for the week at 13.000 million barrels per day. Production last year at the same time was 12.100 million barrels per day.

- Imports decreased to 6.117 million barrels from 6.539 million barrels per day compared to 6.540 million barrels per day last year.

- Crude exports from the US decreased to 3.850 million barrels per day from 4.378 million barrels per day last week compared to 2.888 million barrels per day a year ago

- Canadian exports to the US decreased to 3.357 million barrels a day from 3.802 million barrels per day last week

- Refinery inputs increased during the week to 15.838 million barrels per day

- As at March 20, 2020, US natural gas in storage was 2,005 billion cubic feet (Bcf), which is 17% above the 5-year average and about 79% higher than last year’s level, following an implied net withdrawal of 29 Bcf during the report week

- Overall U.S. natural gas consumption fell by 1% during the report week.

- Production was flat for the week. Imports from Canada rose 6% from the week before. Exports to Mexico were up 1% week over week.

- LNG exports totaled 55 Bcf

- As of March 6, 2020, the onshore Canadian rig count decreased 42 to 54 (AB – 46; BC – 7; SK – 1; MB – 0; Other – 0). Rig count for the same period last year was 87.

- US Onshore Oil rig count at March 27, 2020 is at 624, down 40 from the week prior.

- Peak rig count was October 10, 2014 at 1,609

- Natural gas rigs drilling in the United States is down 4 at 102.

- Peak rig count before the downturn was November 11, 2014 at 356 (note the actual peak gas rig count was 1,606 on August 29, 2008)

- Offshore rig count was down 1 at 18.

- Offshore peak rig count at January 1, 2015 was 55

US split of Oil vs Gas rigs is 86%/14%, in Canada the split is 66%/34%

Trump Watch: GM sucks – still want to test the engine. Fake news.

Kenney Watch (new!): After the energy bailout, who am I going to complain about?

Trudeau Watch (for balance): Gonna bail out the oil sector, please no one tell my dad